Understand what drives your premium

Your car insurance premium is the annual price the insurer charges to carry your risk. It is set by rating factors, and small changes to any of them can move the quote noticeably.

Age and driving experience. The ABI says younger drivers, particularly those under 25, pay the highest premiums because claim frequency and severity sit at the top of the curve for that age group.

Vehicle type and use. Small city cars like the Ford Ka, Volkswagen Up! and Hyundai i10 sit in the lowest insurance groups and are the cheapest to cover. Higher-performance cars attract higher premiums.

Driving history. A clean licence with no at-fault claims translates into lower quotes. No-claims discount is the single biggest lever you control over time.

Location. Postcode is a heavy rating factor. Urban areas with higher claim frequency and theft rates cost more to insure than rural Northumberland addresses. Learn more about insurance groups in our used car buying guide.

Understand compulsory vs voluntary excess

Excess is the first slice of any claim you pay before the insurer pays the rest. Every policy has a compulsory excess, and most let you stack a voluntary excess on top in exchange for a lower premium.

Compulsory excess is set by the insurer based on your age, vehicle group and licence. You cannot negotiate it.

Voluntary excess is yours to choose. A higher voluntary excess can bring meaningful savings, but only set it at a level you can comfortably pay on the day of a claim. Never set a voluntary excess higher than your emergency savings.

Pick the right coverage type

UK motor policies come in three headline tiers. The right one is usually not the one with the lowest-sounding name.

Third Party Only (TPO). The legal minimum. Covers damage or injury you cause to other people or their property. Does not cover your own car.

Third Party, Fire and Theft (TPFT). Adds protection against your car being stolen or damaged by fire, but still leaves you exposed for at-fault accidents to your own vehicle.

Fully Comprehensive. The highest level of cover. Includes damage to your own car regardless of fault, plus the Third Party and Fire/Theft protection above.

Cut your premium without cutting cover

The biggest savings come from a combination of small moves, not one magic trick.

Add an experienced named driver. A parent, partner or older sibling with a clean licence can bring the quote down. The main driver on the policy must be the person who drives the car most. Mis-stating this is called "fronting" and it is insurance fraud under the Fraud Act 2006.

Choose a car in a low insurance group. Vehicles in insurance groups 1-5 are the cheapest to cover. Examples include the Ford Ka+, Volkswagen Up!, Hyundai i10, Kia Picanto and Skoda Citigo.

Build and protect a no-claims bonus. The Association of British Insurers notes that a protected no-claims discount can reach around 60-65% after five claim-free years (source: ABI). Protect your NCB for a small additional premium so it survives a single claim.

Secure the car. Approved alarms, immobilisers and off-road overnight parking all feed into the premium calculation.

Estimate mileage accurately. Over-stating your annual mileage pushes the price up for no reason. Under-stating risks your claim being challenged. Use your MOT history as a reference.

Pay annually if you can. According to the FCA, monthly premium finance is regulated credit and carries interest. Paying your car insurance annually rather than monthly typically avoids a credit charge of around 8-15% on the same cover (Which? and MoneyHelper guidance).

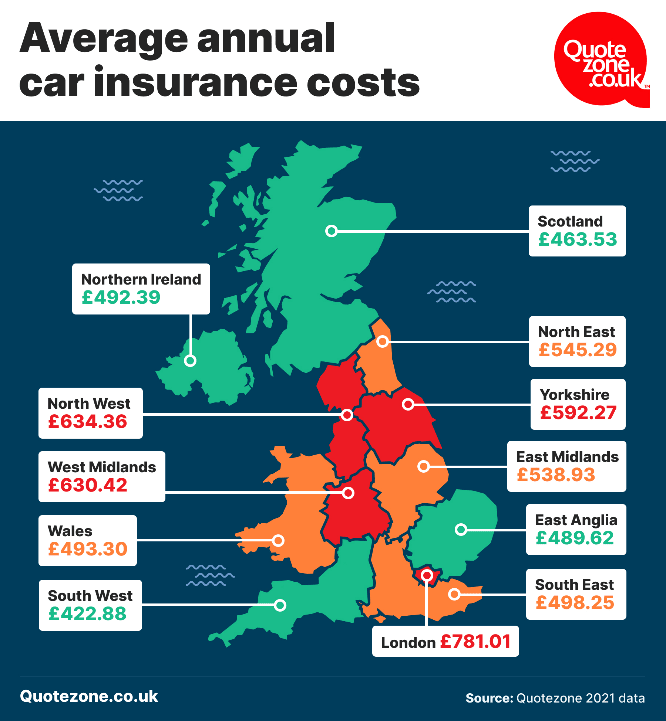

How your postcode changes the price

Insurers price risk by postcode. Dense urban centres with high theft and accident claim rates sit at the top of the scale. Rural Northumberland and the Scottish Borders typically sit much lower.

If you move, update your insurer immediately. A failure to disclose a postcode change is a breach of the duty of fair presentation under the Consumer Insurance (Disclosure and Representations) Act 2012 and can void a claim.

Understand how age and experience affect cost

Age matters because claim data follows a U-shape. Drivers aged 17-24 and drivers over 75 sit higher on the risk curve. Drivers in their 40s and 50s with long clean licences pay the least.

Black box telematics is most valuable for the under-25 group because it lets safe drivers prove they do not fit the statistical average for their age band.

Other factors that change your quote

Occupation. Your job title feeds into the rating engine. Office-based roles typically cost less to insure than occupations with high road mileage.

Vehicle modifications. Any non-standard alteration, from remapped ECUs to aftermarket alloys or cosmetic body kits, can push the premium up and must be declared. Undeclared mods can void a policy entirely.

Driving habits. High annual mileage, long commutes, and telematics data that shows heavy braking or late-night driving all affect the price.

Telematics cover. A black box or app-based policy monitors speed, braking, cornering and time of day. For cautious drivers, especially those aged 17-24, it can shave a meaningful amount off renewal quotes.

Thinking about the total cost of ownership?

Insurance is only one line on the running cost sheet. Read our complete finance guide, see what we have recently sold, or get a free valuation with our sell car wizard.

About the author

John James is a car dealer in Hexham who helps customers understand the full running costs of car ownership, including insurance, before buying.